A genuine warning in the face of a situation that has become, in its view, increasingly worrying. On April 9, during its traditional annual press conference, held remotely this year, Copacel sounded even more alarmist than in previous years. The trade association, which represents French producers of pulp, paper, and board (74 companies, employing nearly 10,000 people), highlighted “the increasing number of paper mill closures over the past 24 months, as well as the precarious situation of several sites at the start of 2026.” These indicators, according to the association, highlight “the urgent need to implement an ambitious policy to promote reindustrialization.”

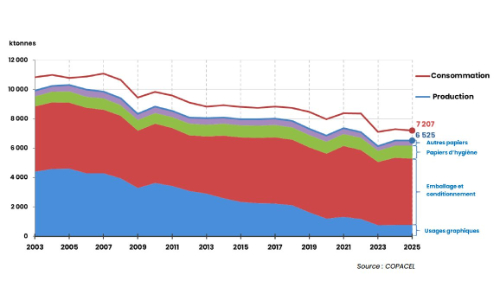

In 2025, France produced 6.525 million tons, marking a slight decline (-0.1%, or 4,000 tons less), while the European average was more heavily impacted with an estimated decrease of 1.5%. French revenue fell by 3% to €5.6 billion. French apparent consumption of paper and board declined by 1.2% to 7.2 million tons. The output of packaging and wrapping papers and graphic papers decreased by 1.2% (to 4.51 million tons) and 2% (to 770,000 tons), respectively. Conversely, sanitary and household (tissue) papers increased by 7.5% to reach 889,000 tons. Other papers and boards (specialty products, etc.) also saw positive growth (+1.2% to 352,000 tons).

A worrying trend of closures and weakening of the sector

In the space of 15 months, since January 1, 2024, seven paper mills, out of a total of 81, have permanently ceased operations in France. These site closures have serious consequences for employment, wealth creation, regional development, and industrial sovereignty (France is structurally a net importer of pulp, paper, and board). Furthermore, two companies that produce packaging paper (i.e. Cenpa and Gemdoubs, Editor’s note) are currently in receivership, while Fibre Excellence (which operates two pulp mills, in Saint-Gaudens and Tarascon, Editor’s note) is engaged in conciliation proceedings, which are expected to conclude by April 15.

Furthermore, according to Copacel, “several other companies exhibit vulnerabilities that could worsen due to the combined effects of falling selling prices, insufficient equipment utilization, and rising production costs”. However, as Paul-Antoine Lacour, Copacel General Manager of Copacel, pointed out, « the closure of paper mills in France is explained less by a drop in demand than by the difficulties French companies face in withstanding increasingly intense international competition. »

Clearly identified structural causes

According to Copacel, several factors explain this deindustrialization. On the one hand, in some segments, overcapacity among foreign producers encourages the importation of products (particularly from China), sometimes at prices lower than production costs in France. This pressure is amplified, for some paper grades, by American tariff barriers, which redirect volumes initially intended for the United States to the European market. On the other hand, France is still struggling to improve the competitiveness of its “heavy” industries (due to the burden of production taxes, energy costs, and administrative complexity), resulting in production costs higher than those of competing countries.

In these conditions, even more challenging than in previous years, Copacel « calls for the swift implementation of measures at both the EU and national levels, as the government’s rhetoric on reindustrialization must be followed by concrete actions » :

- strengthening of mechanisms to protect the European market,

- reduction of production taxes,

- leveraging the competitive advantage of the French nuclear power plant fleet (post-ARENH mechanism),

- development of a forestry policy more focused on its economic function,

- simplification of the regulatory framework (EPR, PPWR, EUDR),

- adaptation of environmental requirements to companies’ investment capacities (water charge, CO₂ quotas).

“The paper industry provides our citizens with products that are both traditional and innovative, contributing to the fight against climate change and the development of the circular economy,” explained Christian Ribeyrolle, President of Copacel. Faced with the growing risks to the long-term viability of many sites, it is urgent to implement an ambitious industrial policy that serves the competitiveness of our industry and the sovereignty of our country.”

The April-May issue (No. 402) of “La Papeterie Mag” will provide a full report on these figures and trends.

Valérie Lechiffre

RELATED NEWS